TL;DR: Jobtech Alliance invested in Flowcart and Bumpa because they are building the missing operating layers for African commerce. Flowcart structures supply and distribution. Bumpa structures daily operations. Together, they make MSMEs more productive and income more predictable.

In Nairobi, a retailer like Wanjiku loses significant potential earnings because she can’t predict when her stock will run out. In Lagos, a social commerce merchant like Zainab spends hours daily manually verifying bank transfers and coordinating erratic delivery riders.

For the 80% of Africans employed by MSMEs, operational complexity (often, sheer chaos) is the biggest barrier to growth and livelihood sustainability. Meanwhile, small shops will continue to account for 65-75% of retail sales in many African markets until 2030. Traditional e-commerce storefront models often fail because they ignore how African commerce actually functions: via conversation, informal trust, and very fragmented logistics.

For most Africans, a livelihood is not earned through a formal job in an office, it is through running a small business, riding dispatch, or doing small trade every day. Sub-Saharan Africa has about 44 million MSMEs, and 97% of them are microenterprises. The informal sector accounts for over 80% of jobs. Therefore, positively impacting MSMEs and commerce operations in Africa has an impact on the livelihoods of many Africans at scale.

Why we invested

Our investment in Flowcart and Bumpa is rooted in a landscape scan we conducted on digital services for microenterprises in Sub-Saharan Africa. In MSME markets, impact does not come mainly from adding more users. It comes from helping each business sell more, waste less time, and operate more efficiently. When stockouts reduce and payments are easier to track, revenues rise, and income becomes more sustainable. This helps these businesses to hire more workers, retain staff, and extend hours for their workers.

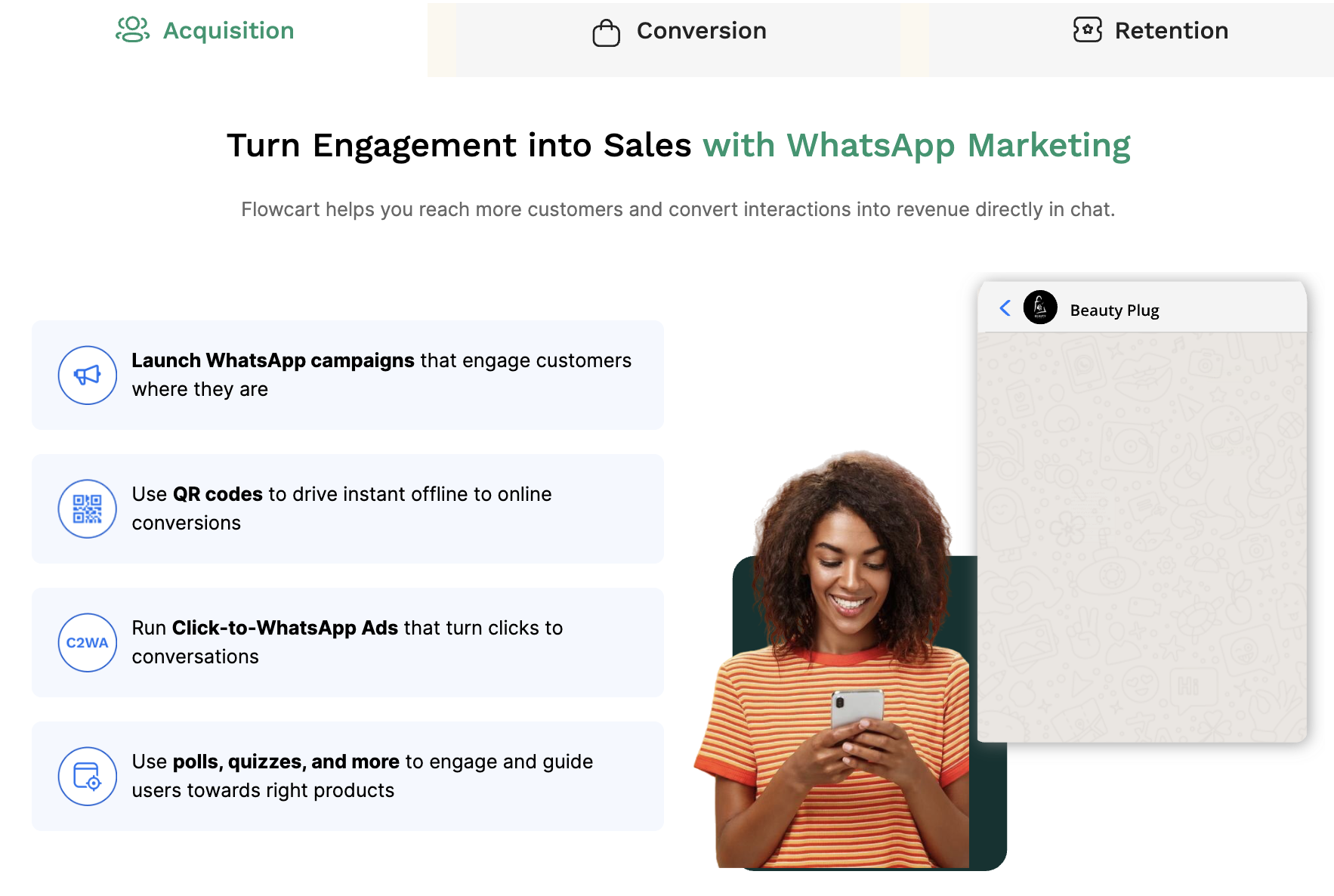

There is a clear opportunity in augmentation, platforms that improve how entrepreneurs run existing businesses, rather than just intermediation. The traditional centralised e-commerce model has struggled to scale due to low trust and poor infrastructure, which jobtech platforms can solve by leaning into social media (WhatsApp, Instagram) and local agent networks that solve the trust and last-mile challenges

MSMEs in Africa face persistent constraints related to productivity, predictability, and access to finance. In most cases, these constraints are not driven by a lack of customers but by the difficulty of managing transactions, relationships, and information across fragmented systems. A lot of existing solutions focus on visibility and access to customers: storefronts, catalogues, or checkout experiences designed to mirror global ecommerce models. But sales often close through conversation rather than checkout.

In this context, where can jobtech platforms make a difference? We believe the most effective infrastructure will be built around existing behaviour, not in opposition to it. So platforms need to respect existing behaviour and focus on introducing structure beneath it. What does this structure look like? On the one hand, providing entrepreneurs with streamlined data for decision-making, and secondly, by creating predictability in supply chains and fulfilment.

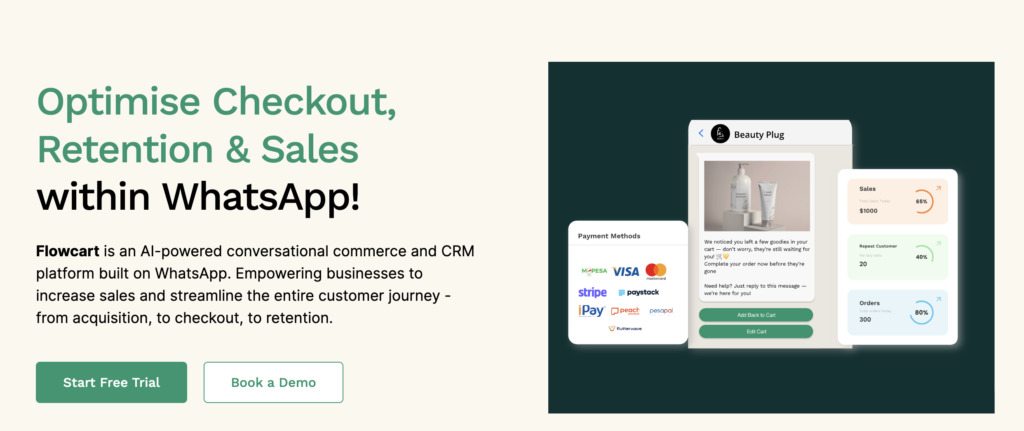

Flowcart: making informal distribution legible

Flowcart (formerly Sukhiba) stood out to us because it started from how informal distribution actually works. It did not try to retrain retailers or force apps. It treated WhatsApp as the place where ordering already happens, then turned those conversations into records that brands and distributors can use. Retailers keep ordering the same way, while Flowcart captures what was ordered, what was delivered, what repeats, and how incentives are earned.

Women own over 40% of SMEs in Africa, yet face a financing gap of about $42 billion. Many women-led businesses sell consistently but still cannot access credit because they lack the records lenders trust. Flowcart helps by leveraging everyday business transactions into a financial record. When a shop reorders, that becomes a trackable signal. Repeat orders show demand. Basket size shows capacity. Payment behaviour shows reliability. This is how daily trade stops being invisible and starts becoming something lenders can underwrite.

This is already happening at scale. By October 2023, Flowcart was working with more than 30 distributors, reaching around 15,000 SMEs. By August 2024, that footprint had grown to over 35,000 SMEs across eight markets. As more shops transact through the platform, more merchants build the record they need to access working capital, and more households benefit from steadier sales and more predictable income across the distribution chain.

Bumpa: stabilising operations at the point of sale

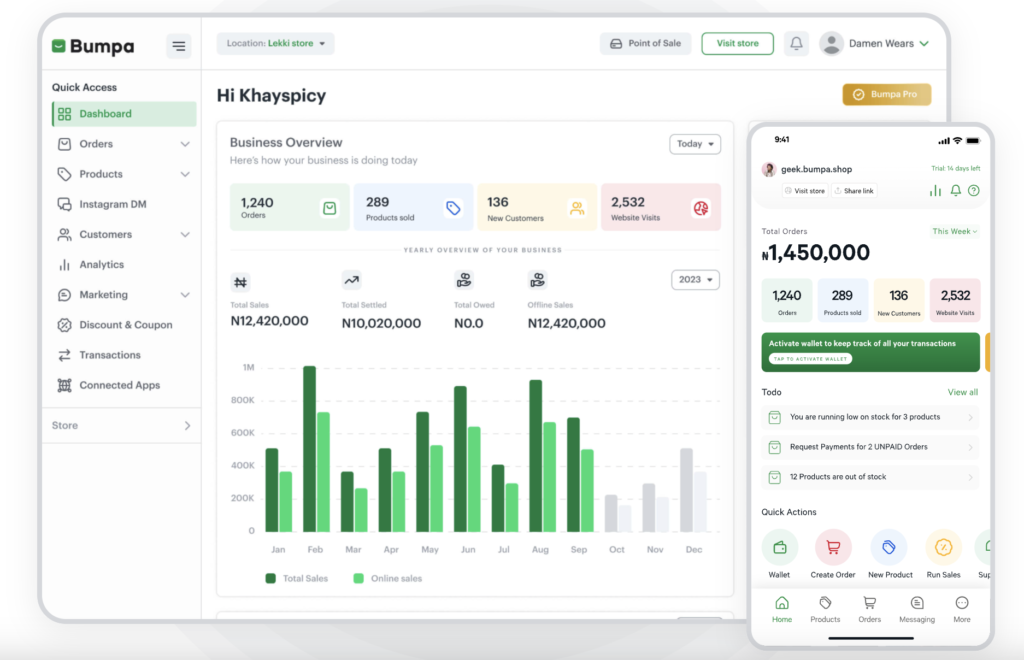

In Nigeria and now Kenya, Bumpa is becoming the operating system for merchants selling online. Small businesses do not just sell in one place. They sell on WhatsApp, Instagram, sometimes a website, and increasingly across multiple channels at once. To manage that, they often stitch together different tools for payments, logistics, inventory, and sometimes even credit.

Bumpa reduces the fragmentation that stops small businesses from growing. Orders that previously sit in DMs, payments that often arrive as screenshots, and delivery updates that are unpredictable no longer exist. When orders, payments, stock, and delivery are managed in one place, merchants spend more time selling. This allows these businesses to grow and bring in more help, even if it is one person for packing, customer follow-up, or delivery coordination. Over time, better operations do not just improve sales. They make work more stable for the merchant and for the small team around them. Over time, fewer mistakes turn into more trust, and more trust turns into repeat buying and steadier income. By 2022, Bumpa had completed 200,000+ orders and crossed $20 million in GMV. It was trusted by 50,000+ small business owners at the time. By 2025, Bumpa was supporting 100,000+ businesses and managing millions of orders.

Lessons learned

We need tech and touch. Flowcart showed us that conversations that began online only moved when someone showed up physically. Procurement in FMCGs is still trust-heavy. So sales need to be hybrid by default. The tech platforms open the doors, while the physical presence unlocks them.

Positioning is critical. When Flowcart was described as “WhatsApp commerce,” many buyers and users first interpreted it as another messaging tool or another marketing tool. However, when the platform began positioning itself as a revenue driver, showing how it can drive repeat orders and reduce missed restocks, the conversation changed.

Banks and lenders value trusted merchant data. When cleaned properly, it can serve as a financial record for lending, especially for businesses in the informal economy. During our venture support, we engaged multiple lenders and saw strong demand to pilot credit using Flowcart’s transaction data. The majority moved beyond introductory conversations to NDAs, data-sharing discussions, and pilot design conversations to test this out. When you can show real data on how merchants buy, reorder, and pay, lenders are way more willing to lend.

In a new geography, presence in the community is non-negotiable. Bumpa in Kenya showed us that while paid ads and social media campaigns created awareness, on-ground agents are what brought in paying merchants. If payments felt unusual or complicated, trust dropped fast. Early sign-ups also did not automatically become paying users. What accelerated the market entry was hands-on onboarding through WhatsApp and community groups.

What next

Both companies have now moved past the early testing stage. They have users who pay and use their platforms consistently. Their focus is now on scale.

For Bumpa in Kenya, the next 6–12 months will be defined by market expansion. The priority is to onboard merchants who process 50–100 orders per month through WhatsApp and social channels, but still reconcile their payments and inventory manually. Early progress shows strong interest from Kenyan businesses, but slower paid conversion. The immediate goal is to build a stable base of paying merchants with clear 30-day activation targets, before scaling marketing spend.

For Flowcart, the next step is to embed credit across the markets where it already operates by partnering with lenders and using reorder frequency, basket size, and repayment behaviour as underwriting signals. Rather than requiring traditional collateral, loans will be tied directly to stock purchases flowing through the platform. This unlocks working capital for retailers who are already active, while increasing their reorder volume.